Activity

-

NAFA Administrator posted an articleJETNET releases their fifth edition of the JETNET iQ Market Barometer see more

NAFA member, JETNET released their fifth edition of the JETNET iQ Market Barometer. This edition reviews market performance on a trailing twelve-month basis.

The first half of 2026 was a continuation of business aviation operating from a buoyed baseline post-pandemic. This report examines the current state of the business aviation market in detail, including demand, supply, pricing, and economic trends, to provide a clear picture of where the industry stands and what lies ahead for the remainder of 2026.

View the Complete July Edition hereThis report was originally published by JETNET on July 29, 2026.

-

NAFA Administrator posted an articleBusiness Aviation Q2 2026: Navigating the Supply-Driven Ceiling see more

NAFA member Shawn Holstein, President of Holstein Aviation, shares his recent blog about business aviation in Q2 2026.

The business aviation market in Q2 2026 is telling a fascinating story of resilience matching up against industrial constraint. Demand from passengers and buyers hasn’t slowed down, but the industry is bumping up against a “supply-driven ceiling.” Growth isn’t being limited by a lack of interest, but rather by OEM production bottlenecks and a heavily congested maintenance, repair, and overhaul (MRO) sector.

Here is a breakdown of the key trends shaping the market this quarter.

FLIGHT ACTIVITY: THE WHEELS KEEP TURNING

Flight hours are still on the rise, proving that the operational demand for business aircraft remains a core priority for corporations and individuals alike.

- Sustained Growth: North American flight activity is projected to climb 1.9% in 2026, on track to hit roughly 5.5 million flight hours.

- Sector Performance: Fractional and charter operators are leading the charge. Confidence is high, with 91% of operators expecting to fly the same or more than they did in 2025.

- Regional Hotspots: While the U.S. remains the dominant global market, specific regions are outperforming the baseline. Major aviation hubs like Florida and Texas are seeing year-over-year activity jumps of 2% to 3%.

This article was originally published by Holstein Aviation on July 10, 2026.

-

NAFA Administrator posted an articleAero Asset Releases their 2026 Half Year Heli Market Trends - Single Engine Edition see more

NAFA member Aero Asset released their 2026 Half Year Heli Market Trends - Single Engine Edition.

Heli Market Trends compiles YTD 2026 performance of 4 single engine models in production and variants with recent preowned sales activity. Market performance is ranked from most to least active.

Download full Market Report here

This Market Report was originally published by Aero Asset on July 15, 2026.

-

NAFA Administrator posted an articleJETNET releases their latest edition of JETNET iQ Market Monitor see more

NAFA member JETNET releases Edition 4 of JETNET iQ Market Monitor.

Conflict Cuts Middle East Activity 19%, But Global Bizjet Demand Just Hit a Record

Global business jet departures grew 5.1% over the last twelve months and US corporate profits hit a record high, while the ultra-wealthy population that drives most of the industry’s demand is also at an all-time high. By almost any headline measure, the market through May 2026 looks healthy.

And yet, the energy shock that began earlier this year seems to have some negative impacts on the market, and it is still working its way through the system. Fuel costs have posted their sharpest spike since 2022, consumer sentiment has hit a record low, the Middle East (a small but fast-growing market until February), has been stifled, and pre-owned transaction velocity, running above 15% year-over-year in December, has decelerated to low single digits.

Both narratives can be true at the same time, and the full Market Monitor aims to join them together by joining JETNET’s serial-number-level asset data with WINGX’s tail-level flight activity. Here is how the four chapters read on a May 2026 trailing-twelve-month basis.

This report was originally published by JETNET on July 2, 2026.

-

NAFA Administrator posted an articleJETNET Releases the Third Edition of the JETNET iQ Market Monitor see more

NAFA member JETNET has released the third edition of the JETNET iQ Market Monitor. This edition reviews market performance on a trailing twelve-month basis.

Q1 data and early 2026 trends have introduced some meaningful shifts since our last edition. Download the report to see what's changed across macro, activity, market, and inventory.

What the new data shows:

- Global business jet departures totaled 3.9 million on an April 2026 TTM basis, up 4.9%, with North America accounting for 71% of worldwide activity

- Latin America (+9.8%) and Africa (+13.0%) led regional growth, while the Middle East contracted 17.1% YTD following the February conflict outbreak

- Global bizjet deliveries totaled 769 on an April 2026 TTM basis, pulling back from the 818 units delivered in full-year 2025, though OEM order books remain at decade-highs

- The April 2026 TTM pre-owned transaction trend rose above 15% YOY in December 2025, before softening to just +2% in April 2026 as the Middle East conflict and macro uncertainty weighed on buyer confidence

- Regions outside North America and Europe accounted for almost 15% of global departures TTM, with the Middle East seeing fuel uplift running more than 40% below pre-conflict norms, though with tentative signs of recovery in recent weeks

The 2026 GDP forecast has been revised down to 3.1%, reflecting trade tensions and the Middle East conflict. US corporate profits hit all-time highs, and equity markets remain volatile following shocks from the Strait of Hormuz closure.

Download JETNET iQ Market Monitor's third edition here

This report was originally published by JETNET on June 1, 2026.

-

NAFA Administrator posted an articleGAMA Releases First Quarter 2026 Aircraft Shipment and Billing Report see more

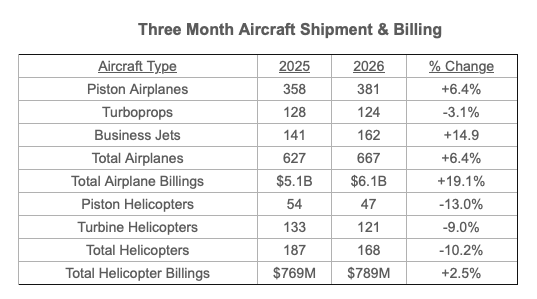

WASHINGTON, D.C. – On May 28, 2026, the General Aviation Manufacturers Association (GAMA) published the first quarter 2026 General Aviation Aircraft Shipment and Billing Report. The results for the first three months of 2026, when compared to the same period in 2025, show increased shipments in the piston airplane and business jet sectors and an increase in the overall value of aircraft shipments.

Aircraft shipments through the first quarter of 2026, when compared to the same period in 2025, saw piston airplanes increase 6.4% with 381 units, turboprops decrease 3.1% with 124 units, and business jets increase 14.9% with 162 units. The value of airplane deliveries through the first quarter of 2026 was $6.1 billion, an increase of 19.1%.

Helicopter shipments through the first quarter of 2026, when compared to the same period in 2025, saw piston helicopters decrease by seven units to 47, and turbine helicopters decrease by 9.0% with 121 units. The value of civil-commercial helicopter deliveries was $789 million.

GAMA’s complete 2026 first quarter report can be found at gama.aero.

This Press Release and report were originally published by GAMA on May 28, 2026.

-

NAFA Administrator posted an articleGlobal Jet Capital Releases Q1 2026 Market Brief see more

NAFA member Global Jet Capital releases their Q1 2026 Market Brief.

While the geopolitical situation contributed to economic uncertainty in Q1, market fundamentals remained healthy. The quarter showed strong demand for business aviation, reflected in increasing aircraft departures, OEM backlog, and stable pre-owned availability. Transaction levels declined year over year in Q1 as a result of supply chain constraints and comparison with a strong Q1 2025. Delays in data reporting have also impacted transaction levels. The business jet market is expected to remain resilient throughout the remainder of 2026.

- In Q1 2026, the global economy remained resilient with steady GDP growth of 2.7 percent despite the conflict in the Middle East.

- Business jet departures experienced broad-based growth in Q1, rising 3.8 percent year over year.

- OEM backlogs rose 19.3 percent year over year in Q1 2026, reaching $57.1 billion for the four OEMs that reported Q1 results.

- Transaction activity was softer in Q1, largely reflecting timing-related delays in data reporting.

- Pre-owned aircraft available for sale as a percentage of the total installed base was lower in Q1 2026 than Q1 2025, declining to 6.7 percent from 7.2 percent.

- In Q1 2026, bluebook values increased 1.1 percent, reflecting modest industry-wide appreciation on a year-over-year basis, although there was variance across segments and models.

This report was originally published by Global Jet Capital on May 27, 2026.

-

NAFA Administrator posted an articleAMSTAT releases their 2026 Q1 Preowned Business Aircraft Market Report see more

NAFA member AMSTAT releases their 2026 Q1 Preowned Business Aircraft Market Report.

The latest data from AMSTAT, sourced through the AMSTAT Premier+ platform, indicates that the preowned business aircraft market remained strong in Q1 2026. Preowned business aircraft transactions in Q1 2026 declined by 10.5% compared to Q1 2025. This decrease should not be interpreted as a market slowdown, as Q1 2025 represented an unusually strong quarter that significantly exceeded prior-year activity. Even with this year-over-year decline, Q1 2026 transactions surpassed the 10-year Q1 average by 4%.

Highlights (see Report for segment breakdown):

Business Jets:

Preowned business jet transactions in Q1 2026 were down 11.4% compared to Q1 2025, mirroring trends in the broader market. However, activity remained strong, exceeding the 10-year Q1 average by 9.1% and surpassing Q1 transaction levels in both 2023 and 2024.

Business Turboprops:

Preowned turboprop transactions in Q1 2026 declined by 8.9% compared to Q1 2025 and were 4.8% below the 10-year Q1 average. However, activity exceeded Q1 2024 levels and was consistent with Q1 2023.

This report was originally published by AMSTAT on May 4, 2026.

-

NAFA Administrator posted an articleJETNET releases their latest edition of JETNET IQ Market Monitor see more

NAFA member JETNET releases their second edition of the JETNET IQ Market Monitor.

Q1 data has shifted a few of the patterns we previously flagged, and there are segments where the picture looks meaningfully different from what we reported. Download our latest report to see what's changed.

What the new data shows:

- Global bizjet departures reached 3.9 million on a trailing 12-month basis, up 5.0% YOY — but the Middle East contracted 11.4% in Q1 2026 following the February conflict outbreak

- The pre-owned transaction trend recovered to +16% YOY in December 2025, then softened to just +1% by March 2026 as macro uncertainty weighed on buyer confidence

- New deliveries eased to 750 units TTM, pulling back from 809 units in full-year 2025 — though OEM order books remain at decade-highs

- Latin America (+11.3%) and Africa (+13.0%) led regional growth, while emerging markets now account for nearly 15% of global departures

The macro backdrop has shifted too. The 2026 GDP forecast has been revised down to 3.1%, equity markets retreated from late-2025 highs, and Middle East fuel uplift is running more than 40% below pre-conflict norms with no recovery trajectory yet visible.

This report was originally published by JETNET on April 30, 2026.

-

NAFA Administrator posted an articleAero Asset Reports Tightening Supply and Firm Pricing in 2025 Twin-Engine Helicopter Market see more

ATLANTA, USA, March 10, 2026 – Aero Asset, a global helicopter sales and market intelligence firm, has released its 2025 Annual Heli Market Trends Twin-Engine edition during a press conference at VERTICON in Atlanta, GA. Backed by Aero Asset’s expertise and proprietary market insight, this report delivers a comprehensive analysis of the global preowned twin-engine helicopter market in 2025.The report tracks activity across weight classes, configurations, and regions, as well as trends in sales, supply, pricing, and liquidity. At the end of 2025, the data revealed that twin-engine supply dropped by 26% year-over-year (YOY), reaching a new five-year low.

Download 2025 Annual Heli Market Trends Twin-engine Edition here.

This report was originally published by Aero Asset on March 10, 2026.

-

NAFA Administrator posted an articleGlobal Jet Capital Releases Q4 2025 Market Brief see more

NAFA member Global Jet Capital releases Q4 2025 Market Brief.

The business jet market was on solid footing in Q4 2025. With a positive macroeconomic environment, business jet market fundamentals remained strong, including rising usage and transaction activity and steady aircraft availability and values. These trends supported the market’s stability and set the stage for continued momentum into 2026.

- Following uncertainty earlier in the year, the global economy continued to grow in Q4 2025, and some economists have upgraded their growth expectations.

- Business jet departures experienced broad-based growth in Q4, rising 4.6 percent year over year.

- OEM backlogs rose 10.4 percent year over year in Q4 2025 as industry-wide orders increased.

- Transaction activity was strong in 2025, with total volume increasing 9.8 percent year over year.

- Pre-owned aircraft available for sale as a percentage of the total installed base was lower in Q4 2025 than Q4 2024, declining from to 6.9 percent from 7.4 percent.

- In Q4 2025, bluebook values increased 0.4 percent, reflecting stability between supply and demand during the quarter.

This market brief was originally published by Global Jet Capital on February 24, 2026.

-

NAFA Administrator posted an articleGAMA Releases 2025 Aircraft Shipment and Billing Report see more

WASHINGTON, D.C. – Today, the General Aviation Manufacturers Association (GAMA) released the 2025 General Aviation Aircraft Shipment and Billing Report during its annual State of the Industry Press Conference. Overall, when compared to 2024, the business jet and piston airplane segments saw increases in shipments and preliminary aircraft deliveries were valued at $35.7 billion, an increase of 14.6%.

“The state of the general aviation manufacturing industry remains steadfast. We continue to see robust numbers of total aircraft delivered as well as annual billings eclipsing $35 billion, the highest it has ever been. While some segments are seeing marginal declines in deliveries, they are all still above 2019 levels. As manufacturers work hard to meet the challenges and demand of today, they remain focused on advancing safety and innovation for the future of the entire aviation industry,” said James Viola, GAMA President and CEO.

Airplane shipments in 2025, when compared to 2024, saw piston airplanes increase by ten units to 1,782, turboprops decline slightly by 5.1% with 594 units, and business jets increase 11.8% with 854 units. The value of airplane deliveries for 2025 was $31.0 billion, an increase of 16.1%.

Click here for full Press Release

This press release was originally published by GAMA on February 18, 2026.

-

NAFA Administrator posted an articleGama Q3 2025 Report Bizjet Shipments Are Booming see more

NAFA member General Aviation Manufacturer’s Association (GAMA) issued its Q3 2025 billings and delivery report and the news in the jet segment was very good indeed. Mike Potts takes a closer look.

The piston market could hardly be more flat, with just five units separating this year’s total from last year’s.

Of the 16 companies reporting piston deliveries, five are ahead of last year’s totals, seven and lagging behind and four are even. Looking at just the third quarter, six are ahead, six are behind and four are even.

While this suggests a balanced market, there is a pretty wide disparity among just how some of the individual companies are doing. Some are doing quite well while others are far off their prior year pace.

Cirrus continues to be the single-engine piston market leader, but by a margin that is narrowing as the year plays out. They finished the third quarter with 483 deliveries, up more than 15.27 percent from the 419 units they reported last year.

Oddly, their third quarter results were very close, with 178 units this year against 175 in 2024, or a gain of just 1.7 percent. Cirrus is so far ahead of the rest of the field that this difference hardly seems to matter, but it is interesting to watch.

This report was originally published by AvBuyer on January 28, 2026.

-

NAFA Administrator posted an articleAero Asset Reports Tightening Supply and Resilient Pricing in 2025 Single-Engine Helicopter Market see more

NAFA member Aero Asset releases their 2025 Annual Heli Market Trends - Single Engine Edition.

Heli Market Trends compiles 2025 performance of 4 single engine models in production and variants with recent preowned sales activity. Market performance is ranked from most to least active.

This report was originally published by Aero Asset on January 27, 2026.

-

NAFA Administrator posted an articleGAMA Q3 2025 Report: Bizjet Shipments are Booming see more

The General Aviation Manufacturers Association (GAMA) issued its Q3 2025 billings and delivery report and the news in the jet segment was very good indeed. Mike Potts takes a closer look.

We are on track for the first 800-unit business jet year since 2019 and, going by the evidence presented in GAMA’s Q3 2025 shipment report, I believe we will exceed 2019’s total of 809 units by a significant margin. Outside of the jet market, results weren’t quite so strong.

Overall, aircraft deliveries for the first nine months of 2025 totaled 2,201 units, an increase of 1.5% over the 2024 Year to Date (YTD) total. These included 554 business jets, 409 turboprops and 1,238 piston-powered airplanes.

The jet total was 10.6% ahead, Year Over Year (YOY) of the 501 units reported in 2024. In contrast, turboprops were off 6.0% from the 435 delivered in 2024 while piston-powered aircraft were up slightly (five units) from 1,233 a year ago.

Billings for the first nine months of 2025 totaled $19.4bn in US dollars, up 13.2% from $17.1bn recorded in 2024.

Business Jet Market Specifics

With revenues up by more than $2bn, you’d naturally assume things must be doing very well in the jet market, but not perhaps as well as you might expect.

Of 10 jet OEMs reporting to GAMA, six enjoyed gains over last year, but three lagged their 2024 performance and one matched it. For Q3 2025 alone, just four OEMs saw positive gains compared to Q3 2024, three were down and three were even. Nonetheless, jet sales are proceeding at a record pace, although there’s been something of a shake-up in the usual order of things.

Textron’s Cessna unit continued to lead the market for jet deliveries, but not by the margin it has enjoyed in the past. Cessna’s YTD total of 123 jets was just four units ahead of its 119 shipments for the same period in 2024. In Q3 alone, Cessna was up by a single unit from 41 to 42.

This article was originally published by AvBuyer on December 15, 2025.